TermCanada

Life Insurance for Diabetics in Canada

Table of Contents

If you’re looking for information on life insurance for diabetics in Canada, then this guide is for you. It’s completely normal to have questions about life insurance, but when you have diabetes, it’s very common to feel unsure about the answers. Many worry that a diabetes diagnosis automatically means higher premiums, fewer choices, or being declined altogether.

In reality, life insurance underwriting decisions are rarely that simple.

Canadian insurers don’t assess diabetes in isolation. They look at what type of diabetes you have, how the condition shows up over time, how it’s managed, whether there are complications, and how it fits into your overall health picture. Remember, two people with diabetes can receive very different outcomes, even if their diagnoses sound similar on paper.

We at TermCanada created this guide to explain how life insurance for diabetics in Canada actually works. Not to sell you a policy, but to help you understand what insurers look at, what options may be available, and what matters most before you even think about applying.

Insulin’s role is to regulate the amount of glucose (sugar) in the blood. Blood sugar must be carefully regulated to ensure that the body functions properly. Too much blood sugar can cause damage to organs, blood vessels, and nerves. Your body also needs insulin to use sugar for energy.

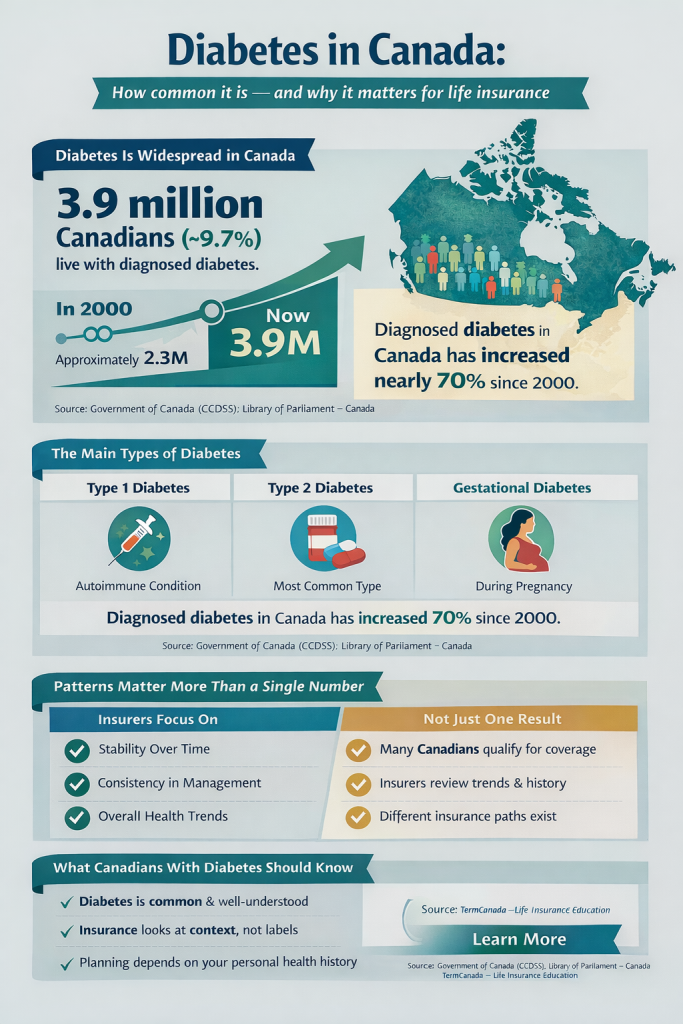

Every 3 minutes one person in Canada is diagnosed with diabetes. Chances are that diabetes affects you or someone you know. What is Diabetes, Diabetes Canada

How Insurers Evaluate Life Insurance for Diabetics in Canada

Life insurance underwriting focuses on long-term risk, not labels. When diabetes is part of an application, insurers are looking for consistency and stability rather than a perfect health history.

They look at patterns over time. A well-managed condition with regular follow-up care is viewed very differently from one with frequent complications or gaps in treatment. This is why outcomes can vary so widely between applicants who have diabetes.

A diagnosis alone doesn’t determine approval. Diabetes is one factor among many, and it’s considered alongside age, lifestyle, family history, and overall health.

So let’s take a closer look at the two most common types of diabetes and key factors in approval.

Life insurance for type 1 diabetes in Canada

Type 1 diabetes is autoimmune in nature and usually diagnosed earlier in life. Because it requires lifelong insulin management, insurers tend to assess it more cautiously than type 2 diabetes.

That doesn’t mean coverage isn’t available.

When it comes to life insurance for type 1 diabetes in Canada, underwriters typically look closely at long-term blood sugar control, treatment consistency, and whether any diabetes-related complications have developed over time.

Applicants who have demonstrated stable management and ongoing medical care may still qualify for traditional term life insurance, although premiums are often higher than average.

When looking for Life Insurance for Diabetics in Canada, what matters most is not the diagnosis itself, but the overall health assessment that has developed alongside it.

Life insurance for type 2 diabetes in Canada

Type 2 diabetes is more common.

From an underwriting perspective, this means there’s a broader range of possible outcomes… not because insurers are inconsistent, but because type 2 diabetes itself presents very differently from person to person.

Some applicants with type 2 diabetes manage the condition primarily through lifestyle changes, such as diet, or with oral medications.

When blood sugar levels remain stable over time and there are no diabetes-related complications, insurers may view the overall risk as moderate and manageable. In this case, it’s possible to qualify for standard or near-standard rates, depending on the rest of the health profile.

Others may require insulin or have additional health considerations, such as high blood pressure, cholesterol issues, or weight-related concerns, which can result in higher premiums.

Across all applications, insurers focus less on isolated test results and more on long-term patterns

Key factors that affect life insurance decisions

When reviewing life insurance applications involving diabetes, Canadian insurers don’t focus solely on the diagnosis. Instead, they assess the big picture to understand long-term risk and overall stability.

Common factors insurers consider include:

Blood sugar stability over time, rather than a single test result

Blood sugar stability over time, rather than a single test result

Age at diagnosis, which helps estimate how long diabetes has been managed

Treatment approach and consistency, including medications and regular follow-up care

Presence or absence of complications, such as kidney, eye, nerve, or cardiovascular issues

Overall health indicators, including blood pressure, cholesterol, weight, and smoking status.

Together, these factors help insurers assess the overall risk of those looking for life insurance for diabetics in Canada. This is why life insurance outcomes can vary even among people with the same diagnosis.

Life Insurance For Diabetics in Canada: Real World Choices

If the underwriting criteria feels overwhelming, this short video explains how Canadian insurers actually assess diabetes in the real world. Long-term patterns rather than single test results matter most. Which is why consistent management is important. While many Canadians with diabetes explore term, simplified, or no-medical options first, permanent life insurance (often called whole life insurance) may also be considered in certain situations. There are multiple coverage paths available, and a diabetes diagnosis alone doesn’t determine the outcome.

Please note: The best life insurance for diabetics in Canada depends on factors such as blood sugar control, treatment history, and the presence of complications.

Life Insurance Pathways for Canadians with Diabetes

Gestational Diabetes in Canada: How It Affects Life Insurance Approval

A1C Target Diabetes Canada: Why Life Insurance Looks at Blood Sugar Patterns, Not One Number

Diabetes in Canada: How Common It Is and What It Means for Insurance

When Will Diabetes Medication Be Free in Canada? What’s Covered and Why It Matters

Life Insurance Options for Diabetes in Canada

Best Simplified Issue Life Insurance Companies Canada – Compare Options

There isn’t a single path to life insurance when you’re living with type 1 or type 2 diabetes. We provided informative articles above to help you with your decision-making process.

Coverage options depend on your overall health profile, how your condition is managed, and how insurers assess long-term stability.

The steps below outline how many Canadians with diabetes move through the decision-making process from understanding their health picture to choosing a coverage option that fits their needs.

Steps for Getting the Best Life Insurance for Diabetics in Canada

Start with your health profile

Life insurance decisions begin with your overall health picture, not a single diagnosis. Insurers look at how your diabetes has been managed over time, whether care has been consistent, and how it fits alongside other health factors. This broader context helps them assess long-term stability rather than isolated results.

The review process

When an application includes diabetes, underwriters focus on patterns, not perfection. They review treatment history, follow-up care, and any signs of complications to understand how stable the condition has been. This is why outcomes can differ even among applicants with similar diagnoses.

Explore your coverage options

Depending on your profile, different types of coverage may be available. Some applicants qualify for traditionally underwritten policies, while others may find simplified issue or no-medical-exam options more appropriate. Each pathway involves different requirements, timelines, and trade-offs.

Read more before you apply

Understanding how these options work in practice can make the process feel far less uncertain for those looking for life insurance for diabetics in Canada. The resources below explain when medical exams may be required, how underwriting decisions are made, and what to consider before choosing a path that fits your needs.

Life Insurance for Diabetics in Canada

Can I qualify for traditional term life insurance?

Yes. Many Canadians with diabetes qualify for term life insurance, particularly when the condition is well managed and complications are minimal or absent.

Term life insurance is often the most affordable form of coverage and is commonly used for income replacement, mortgage protection, or family security during working years. Approval depends on underwriting results, but diabetes alone does not automatically disqualify an applicant.

In some cases, premiums may be higher than average, reflecting the insurer’s assessment of long-term risk. Different insurers also weigh diabetes differently, which is why outcomes can vary.

Simplified Issue & No Medical Exam Life Insurance

If you are one of the many people sifting through all the information connected to life insurance for diabetics in Canada. It’s important to consider all of your options. For some applicants, fully underwritten policies aren’t the right fit. This may be due to complications, complex medical histories, or a preference to avoid medical exams.

Simplified issue and no medical exam policies typically involve fewer health questions and faster approvals. However, these policies often come with trade-offs, including higher premiums and lower coverage limits.

They can be helpful in certain situations for those looking for life insurance for diabetics in Canada, but this process isn’t automatically “easier” or “better.” Understanding the limitations of these products is essential before choosing this route.

Preparing to Apply for

Life Insurance with Diabetes in Canada

Preparation isn’t about trying to present perfect numbers or anticipating an insurer’s decision. It’s about helping the underwriting process accurately and consistently reflect your health.

Life insurance applications involving diabetes are reviewed with a long-term lens. Insurers look at trends over time, how care has been managed, and whether information is complete and up to date. Having a clear picture available can make the review process more straightforward and reduce the likelihood of follow-up requests.

For many applicants, preparation means understanding what information may be reviewed and why it matters. This can help set realistic expectations and make the process feel easier.

Why It Matters

- Shows stability over time rather than a single snapshot

- Demonstrates consistent treatment and follow-through

- Signals ongoing management and medical engagement

- Applying during periods of stable management can support

- Reduces uncertainty and helps set realistic expectations

What to Prepare

- Recent lab results (A1C, blood work)

- Current medications and dosages

- Records of regular follow-up care

- Timing your application thoughtfully

- Understanding underwriting criteria

What preparation helps insurers understand

When diabetes is part of an application, preparation helps insurers see how stable your blood sugar has been over time.

They can also determine whether you are taking care of yourself and whether your treatment has been consistent.

Remember, as with all insurance, they want to understand your overall health, too. Life insurance is all about risk assessment, and if you are in poor health, whether or not you have diabetes, this will be an issue, and your premiums will be higher.

There are many ways to mitigate health issues through quitting smoking, exercising regularly, and maintaining a healthy weight through a sensible diet.

A note on timing and expectation for Life Insurance for Diabetics in Canada

Applying when your diabetes is well managed can support an application, but timing on its own doesn’t guarantee a specific result. Every insurer reviews applications independently and weighs risk in its own way.

Knowing this ahead of time can help reduce frustration and uncertainty for those looking for life insurance for diabetics in Canada. A decision reflects underwriting standards, not how hard someone has worked to manage their health.

How Much Does Life Insurance for Diabetics in Canada Cost?

The cost of life insurance for diabetics in Canada depends on several factors, including the type of diabetes, blood sugar control, medications, age at diagnosis, and overall health. Insurers typically review A1C levels, treatment history, and whether complications are present.

When diabetes is well managed and no major complications exist, many Canadians are still able to qualify for affordable term life insurance coverage. Premiums can vary between insurers because each company evaluates diabetes risk differently, which is why comparing policies can be helpful.

Factors that affect cost include:

• Type 1 vs Type 2 diabetes

• A1C levels and blood sugar stability

• Age at diagnosis

• Medications or insulin use

• Smoking status

• Overall health and complications

Life insurance for diabetics in Canada is more accessible than many people expect. Insurers look at the full health picture, including blood sugar control, treatment history, and overall stability… rather than a diagnosis alone.

While premiums may sometimes be higher than average, many Canadians with well-managed diabetes still qualify for traditional term life insurance, simplified coverage, or other options, depending on their health profile.

Understanding how insurers evaluate diabetes, what factors influence approval, and how different policies work can help you make more informed decisions when exploring coverage.

Frequently Asked Questions

Life Insurance for Canadians with Diabetes

Once you’ve explored how life insurance works for people with diabetes, you may still have questions about coverage types, eligibility, or next steps. That’s completely normal.

The resources below are designed to help you continue learning at your own pace, whether that means speaking with a licensed professional, reviewing how brokers work, or estimating how much coverage might make sense for your situation.

✔Contact a Life Insurance Broker: If you’d like help understanding how life insurance works in practice, a licensed Canadian broker can explain different policy options and how underwriting may apply. Independent brokers work across insurers rather than representing just one company.

✔ How Much Life Insurance Do I Need?: Use our calculator to explore coverage ranges commonly used for income replacement and family protection.

Check out some frequently asked questions we get at TermCanada.

Can people with diabetes qualify for life insurance in Canada?

Yes, Canadians with diabetes qualify for life insurance. Approval depends on the overall health picture rather than the diagnosis alone. Insurers consider factors such as how long diabetes has been managed, treatment consistency, and whether complications are present. Outcomes can vary, but diabetes does not automatically disqualify an applicant.

Does having diabetes always mean higher life insurance premiums?

Not always. Some applicants with well-managed diabetes and no related complications may receive standard or near-standard rates. Others may see higher premiums depending on additional health factors or underwriting results. Each application is reviewed individually, and different insurers assess risk differently.

What’s the difference between type 1 and type 2 diabetes for life insurance?

Type 1 diabetes is autoimmune and typically diagnosed earlier in life, often requiring lifelong insulin use. Type 2 diabetes varies widely and may be managed through lifestyle changes, medication, or insulin. Because of these differences, insurers evaluate type 1 and type 2 diabetes differently, focusing on management history and long-term stability rather than labels.

Can diabetics qualify for term life insurance in Canada?

Yes, many Canadians with diabetes qualify for term life insurance, particularly when the condition is well managed and complications are minimal or absent. Term life insurance is often used for income replacement or family protection and may be available through traditional underwriting or alternative options depending on the applicant’s profile.

What is simplified issue life insurance, and how does it apply to people with diabetes?

Simplified life insurance involves fewer health questions and typically does not require a medical exam. For some people with diabetes, it can be an alternative when traditional underwriting isn’t ideal. These policies often have higher premiums and lower coverage limits, reflecting the reduced medical information provided during the application.

Is no medical exam life insurance the same as guaranteed issue insurance?

No. No medical exam life insurance may still involve health questions, while guaranteed issue life insurance does not assess health at all. Guaranteed issue policies are designed for applicants who may not qualify for other coverage types, but they usually come with lower coverage limits, higher premiums, and waiting periods before full benefits apply.

How do insurers evaluate diabetes during underwriting?

Insurers focus on patterns over time rather than a single test result. They review blood sugar stability, treatment consistency, follow-up care, and whether complications have developed. Diabetes is evaluated alongside other factors such as age, lifestyle, and overall health to assess long-term risk.

Does my A1C level determine whether I’ll be approved?

A1C levels are one factor insurers consider, but they do not determine approval on their own. Underwriters look at trends over time rather than isolated results. Consistency and stability often matter more than a single reading.

Can I apply for life insurance if I have diabetes-related complications?

In some cases, yes. The availability of coverage depends on the type and severity of complications, overall health, and insurer guidelines. Alternative options such as simplified issue or guaranteed issue policies may be available when traditional underwriting is not.

How long does approval take for life insurance applications involving diabetes?

Timelines vary depending on the type of policy. Traditionally underwritten applications may take several weeks, while simplified issue or no medical exam policies provide faster decisions. Timing also depends on whether additional medical information is required.

Should I wait until my diabetes is well controlled before applying?

Applying during a period of stable management can be helpful, but timing alone doesn’t determine outcomes. Every application is reviewed individually. Understanding how underwriting works can help set realistic expectations regardless of timing.

What coverage amounts are typically available for diabetics in Canada?

Coverage limits depend on the policy type and underwriting results. Traditional term life insurance generally offers higher coverage amounts, while simplified issue and guaranteed issue policies tend to have lower maximums. The appropriate amount depends on personal needs and eligibility.

Is working with a broker helpful when applying with diabetes?

Many Canadians choose to work with licensed brokers because they can help explain how different insurers approach underwriting and outline available options. Brokers provide education and comparisons, but applying is always a personal decision.

Subscribe to Our Newsletter

Subscribe to the TermCanada newsletter for expert tips, updates on life insurance options, and innovative strategies to help you protect what matters most. Whether you’re planning for the future or reviewing your current coverage, we’ll keep you in the know, without the spam.

- No pressure. Just practical advice.

- Delivered monthly to your inbox.