Finding the best term life insurance in Canada usually isn’t about choosing ONE company with the “best” policy. The right coverage depends on your age, health, family situation, and how long you need protection.

Most Canadians start exploring term life insurance when they take on major financial responsibilities. A mortgage, young children, or business obligations often raise the question: What would happen to my family financially if something were to happen to me?

Term life insurance is designed to answer that question. It provides coverage for a specific period of time… often 10, 20, or 30 years and pays a tax-free benefit to the people you choose if you pass away during that period.

Because insurers price risk differently, the best approach is usually to compare several companies rather than relying on a single quote.

Canada's life and health insurers provides protection for nearly 30 million Canadians

Why Canadians Buy Term Life Insurance

For many Canadians, term life insurance is about protecting the people who depend on them financially. Young families have many financial challenges. The loss of income from a sudden death can create serious financial pressure. Term life insurance helps reduce that risk by providing a tax-free lump-sum payment to beneficiaries if the insured person passes away during the policy term.

Because coverage lasts for a specific period, such as a:

Term life insurance is typically more affordable than permanent policies. This makes it especially appealing for those who want meaningful protection without a high monthly premium. Many Canadians choose term life insurance to ensure their mortgage can be paid off, their children’s education can be supported, and everyday living expenses can still be covered if the unexpected were to happen.

In simple terms, Canadians are seeking the best term life insurance in Canada for peace of mind. Knowing that loved ones would have financial stability during a difficult time allows families to focus on what matters most, rather than worrying about how bills or debts might be handled.

Term insurance policies don’t include cash value. This means you can’t borrow against your policy. You also won’t get any cash value back if you cancel your policy. You might be able to renew certain term policies.

What Makes a Term Life Insurance Policy the “Best”?

The best term life insurance in Canada isn’t always the cheapest selection. Instead, it’s the policy that provides the right amount of protection at a price that fits comfortably into your monthly budget.

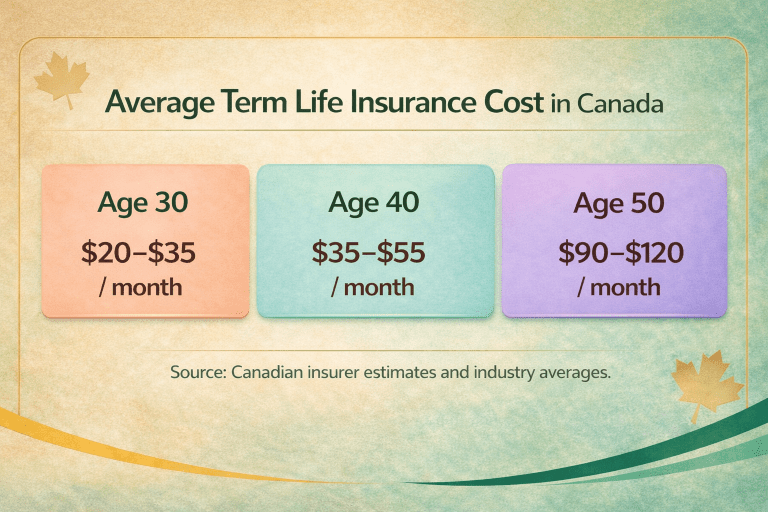

Several factors influence which policy may be the right fit. Premiums vary based on age, medical history, smoking status, and lifestyle. Younger applicants typically pay lower premiums because insurers see them as lower risk.

Flexibility also matters. Some policies allow you to convert your term policy into permanent life insurance later without undergoing another medical exam. For families planning long-term financial security, that option can be valuable.

Finally, the insurer’s financial stability matters. Canada’s life insurance industry is heavily regulated, and most policies are offered by large institutions with long histories in the market.

Several well-established companies dominate Canada’s life insurance market, offering a wide range of term policies and financial strength that Canadians have relied on for decades.

Get your personalized quote below to see available options.

Get your personalized quote below to see available options.